This relocation is not merely a trend; it represents a calculated shift, underpinned by the confluence of skilled labour, a burgeoning domestic market, and enticing government incentives. In this edition of our newsletter, we thoroughly examine this seismic transformation, delving deep into India's rapid ascent as the epicentre of electronic manufacturing.

In several key aspects, India looks to mirror China in terms of its vast scale, robust legal infrastructure, substantial knowledge base, and longstanding tradition of manufacturing excellence. As the world's largest democracy, India's increasingly open economy, coupled with strong incentives in the tech sector, positions it to operate at scale and advance its role as a technological innovator. With this momentum, India aims to move up the value chain and explore long-term prospects in hardware production, including potentially venturing into semiconductor manufacturing.

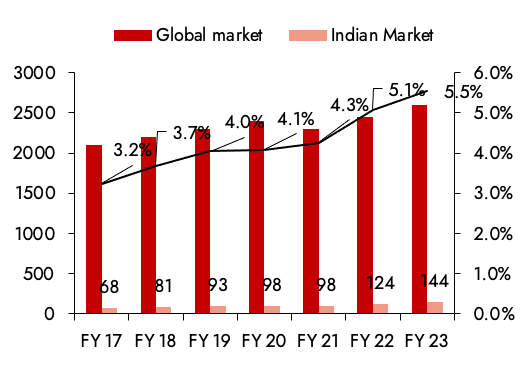

Exhibit 1 - India's share in global electronic manufacturing

Source – Frost and Sullivan report on India’s EMS sector

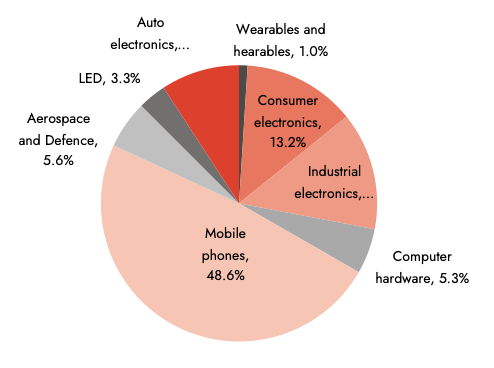

Exhibit 2 - Industry wise contribution to India's EMS sector

Source – Frost and Sullivan report on India’s EMS sector

Exhibit 3 - India’s current 2.8% share in global EMS market to touch 7.3% by FY28E

Source – Frost and Sullivan report on India’s EMS sector

Technology supply chain transformation is not new, with Samsung moving phone production out of China 15 years ago, and rising costs in China and geopolitical risk have already prompted a significant transfer and build-up of production 'around' China, particularly in Vietnam. We expect this trend to accelerate in electronics manufacturing and see India as the next natural major stop for global companies, driven by supportive policies from the Indian government and promising demographics and structural changes.

Apple's interest could send a signal to companies looking to relocate from China. Google is also looking to diversify its production beyond China and Vietnam to India for its Pixel smartphones. Google has discussed its plans with Lava, Dixon Technologies, and Bharat FIH. Interestingly, even HP is looking to ramp up local manufacturing in India.

Exhibit 4 - Many global electronics companies have already started or announced facilities in India

|

Company |

India manufacturing facilities and plans |

|---|---|

|

Apple |

• Indian govt said in Jan-2023 that it expects share of Apple's production from India to rise from 5-7% to potentially 25%. • As per Bloomberg, Apple, through its suppliers Foxconn, Pegatron and Wistron, produced $7bn of iPhones in India in FY23 and exported ~$5bn of those. |

|

Foxconn |

• Commenced India operations in 2015; has three plants, 50+ mobile assembly lines and 25K+ employees. • Investing $500mn to set up a new facility in state of Telangana. |

|

Pegatron |

• As per Reuters, Pegatron plans to set up a second plant in Tamil Nadu just 6 months after opening the first one at $150mn spend. |

|

Samsung |

• Started manufacturing mobiles in India in 2007 and has its plant in Noida, Uttar Pradesh is the world's largest mobile factory. • Plans to invest ~$50mn in Tamil Nadu to manufacture 4G, 5G equipment. |

|

Tata/Wistron |

• As per ET, Tata Group is looking to acquire Wistron's iPhone plant in India. |

|

Dixon |

|

|

Cisco |

• Cisco has its second largest R&D centre outside of the US in India. • Plans to start manufacturing in India, targeting $1bn in combined domestic production and exports in the coming years. |

Source – Google news search

Chip is the new oil. Electronics, and semiconductors as its building blocks, have become critical not only for the economic progress of a nation but also for its national security. India's electronics demand is accelerating, led by rising incomes and digital adoption. Net electronic imports rose to $54bn in FY23, forming 21% of the trade deficit, next only to oil (43%).

Recognizing the rising importance of electronics, the Indian govt has embarked on a path to promote domestic manufacturing. The govt has set a target of raising electronics production to $300bn by FY26 (FY23: ~$100bn), which includes growing exports to $120bn by FY26 (FY23: ~$25bn). While targets seem ambitious, prudent policies have propelled India on the right path with electronics production and exports rising 3-4x in the last 7 years.

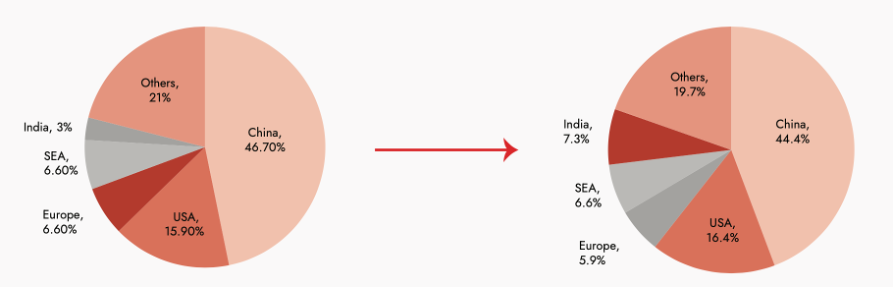

Exhibit 5 - India’s production and export volume targets

Source – MEITY, GOI

WHY WAS INDIA LATE TO THE PARTY?

Though there has been a buzz of Make in India manufacturing, consensus would agree that we are slightly late to the party as India missed building an electronics component ecosystem. The majority of the electronic manufacturing in India is still assembly as India directly evolved from being an agrarian economy to a services-led economy due to a lack of manufacturing thrust from policymakers. Several factors led to this late shift to manufacturing such as:

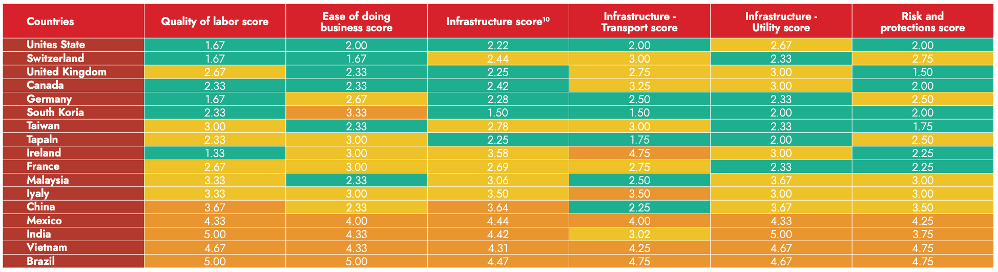

1. India ranked low on qualitative factors despite low cost of factors of production:

In assessing a nation's potential to become a manufacturing hub, cost competitiveness is undeniably a pivotal factor. However, the dynamics at play extend beyond the mere reduction of production costs. India, historically, has faced challenges on multiple fronts that have hindered its ascent in the manufacturing arena. These challenges encompass the intricate interplay of labour skill levels, the ease of doing business, infrastructure reliability, regulatory complexities, and more. Moreover, the ease of doing business, entailing the labyrinth of regulatory intricacies, remains a notable impediment that companies must navigate. This demands streamlined processes, reduced bureaucracy, and a more business-friendly environment.

Exhibit 6 - Global qualitative business development indicators

Source: Cost of Manufacturing Operations Around the Globe, KPMG LLP, 2020

2. Labour laws and lack of an adequately skilled workforce:

Despite having the lowest cost of labour globally, India ranked lower on labour literacy rate availability of skilled labour. Electronic manufacturing is a highly intricate and technology-driven sector that demands a skilled and specialized workforce. The intricate processes involved in designing, assembling, and testing electronic components necessitate a deep understanding of engineering, precision, and quality control. Skilled labour is indispensable for soldering tiny components, programming microprocessors, and ensuring the flawless operation of complex electronic devices. Barely one in five Indians in the labour force were skilled as per the HDR report of 2020, with the figure at 21.2% India stood at 129 among 162 countries as on 2020.

3. Inadequate infrastructure and local component ecosystem:

China and Vietnam have provided infrastructure support like buildings, plug-and-play-type infrastructure, and ready facilities, including onsite dormitories. Strong local presence of sub-assemblies and component ecosystems, whether capex or labour intensive, is an important factor for brands and manufacturers when planning to move production outside China. Currently, China is a global manufacturing hub, with >90% of global electronic products being produced there. This also implies supply chain strength currently located in China, resulting in a peer cluster effect and thus better cost and time to market.

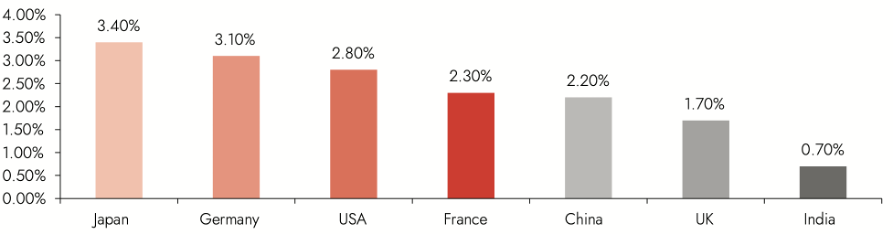

4. Lack of significant investment in R&D:

India historically has been an agrarian and service-led economy and there was a lack of focus on the development of global design and innovation centers. India has attracted some investment in chips and design manufacturing, which has continued. For most other products, the design and intellectual property (IP) rights have been owned by the global parent and the Indian facility has operated a back-end manufacturing site.

Exhibit 7 - R&D spend by major economies as on 2022

Source – World bank report, 2022

HOW ARE WE COURSE-CORRECTING?

As the world ‘de-risks’ i.e., moves supply chains out of China, India is presented with a window of opportunity to realize its long-cherished ambition to become the factory of the world. India’s leaders have thought for decades that the manufacturing-led economic growth model, which served Northeast Asian nations like China, Japan, and South Korea so well, can be replicated in India. Like China, India has an enormous pool of skilled and unskilled labour – a prerequisite to becoming a low-cost manufacturer and exporter.

FOCUS ON ‘MAKE IN INDIA’, TO ‘SELL TO THE WORLD’

The ‘Make in India’ initiative was rolled out to encourage global manufacturers to move their factories to India. The initiative has made India a leading manufacturer of smartphones. Between 2014 and 2022, India shipped 2 billion domestically assembled smartphones and feature phones. In 2022, 98% of phones shipped in India were produced domestically and 16% of such phones were exported. To put this in perspective, in 2014 just 19% of phones shipped in India were domestically assembled. To replicate these countries’ growth trajectories in India, several policies, and initiatives besides ‘Make in India’ are already in play.

PRODUCTION-LINKED INCENTIVE SCHEMES

The Production-Linked Incentive (PLI) – which aims to boost manufacturing in India by giving manufacturers subsidies, has had considerable success. When the PLI was introduced in 2020, it provided subsidies to just 3 categories of manufactured goods. Today, it covers 14 categories, including mobiles. The scheme has seen investments of 6900 crs much higher than the FY24 target of 5500 crs. During the scheme tenure, the scheme is expected to contribute to the production of more than 8 lakh crores, exports of 4.8 lakh crores, and generate more than 200000 jobs.

Exhibit 8 - PLI scheme outlay and companies approved

|

Sector |

Scheme outlay ($ bn) |

Total companies approved |

Key names |

|---|---|---|---|

|

Large scale electronics manufacturing |

5.1 |

32 |

Samsung, Foxconn, Wistron, Pegatron |

|

Auto & auto comps |

3.2 |

95 |

Maruti, Hyundai, M&M |

|

Solar PV modules |

3 |

14 |

Reliance, TataPower, JSW |

|

Advanced chemistry cell |

2.3 |

3 |

Reliance, Ola and Rajesh Exports |

|

IT Hardware |

2.1 |

14 |

Dell, Dixon, Lava |

|

Pharmaceuticals |

1.9 |

55 |

Sun, Dr.Reddy, Lupin, Cipla |

|

Telecom hardware |

1.5 |

42 |

Nokia, Samsung, Syrma, Tejas Networks |

|

Food processing |

1.4 |

182 |

HUL, ITC, Nestle, Dabur |

|

Textile products |

1.3 |

64 |

ABFRL, RWSM, Arvind |

|

Drug intermediaries |

0.9 |

35 |

Aurobindo, Macleods, Granules |

|

Specialty Steel |

0.8 |

27 |

TataSteel, JSWSteel, SAIL, AMNS |

|

White goods |

0.8 |

61 |

Daikin, BlueStar, Havells, Voltas |

|

Medical devices |

0.4 |

23 |

Philips, Panacea, BPL, Siemens |

Source – MEITY, GOI

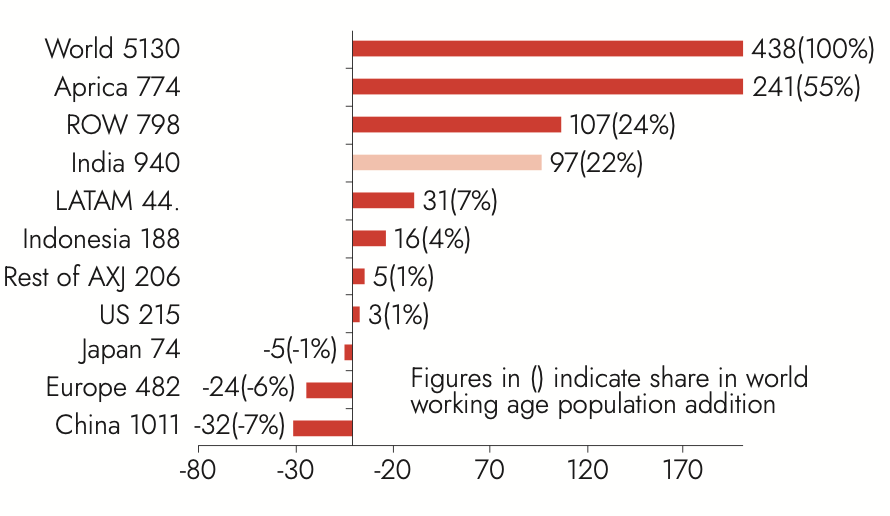

CREATING A SKILLED WORKFORCE

The government’s national skill mission of 2015 is helping the country develop a skilled workforce needed for India to become a thriving 21st-century economy, it needs skilled workers in every sector, including in the tertiary sector. Its objectives are thoughtfully aligned with the government’s vision to transform India into a dynamic thriving modern economy. However, a lot of work is still to be done. To make India an electronic manufacturing and development behemoth, super skills need to be developed and significant investment to be made in R&D spending.

Exhibit 9 - Addition to working age population

Exhibit 10 - India has the highest working age population

FOCUS ON INFRASTRUCTURE DEVELOPMENT

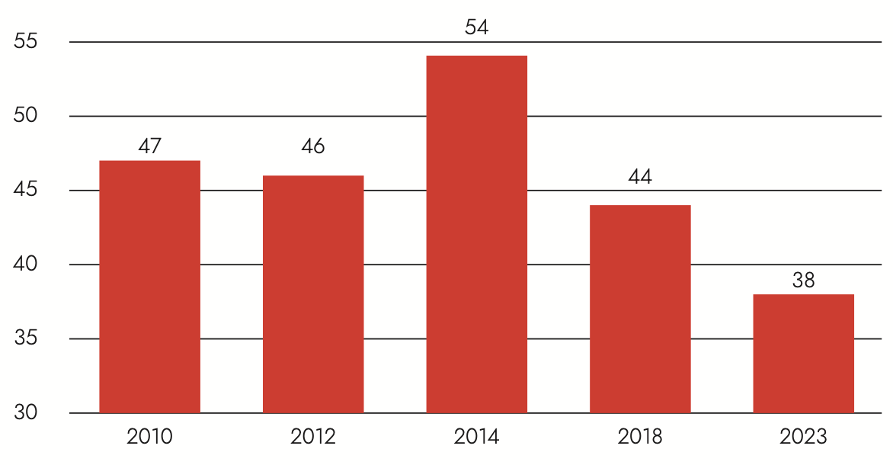

In addition to creating a more skilled workforce, the Indian government is making sweeping changes to address India’s biggest constraint to growth – the country’s poor infrastructure. Today infrastructure in India is being developed at a more robust pace than anywhere in the world – outside China. It’s forecasted that the Indian government will increase capital expenditure on roads from .5% of GDP in 2020 to .8% of GDP in 2023. The country is adding 10,000 km to its highways every year. It’s estimated that India’ will spend 1.7% of its GDP on infrastructure this year – twice as much as the USA and most European countries. The continued building of such infrastructure will lower the cost of transporting items across India and overseas.

Exhibit 11 - India’s ranking in LPI improved to 38 from 2014

Source – MEITY, GOI

A PROTECTIONIST STANCE

Recently, to encourage foreign manufacturers of laptops and other electronics to start manufacturing in India, the Indian government hiked import duties on imported laptops. The import duties will kick in from November 1st, 2023. Following the announcement, 32 entities, including leading manufacturers like Dell, Asus, Foxconn, and HP, have applied for licenses to manufacture laptops, personal computers, and servers in India. Their entry into India will spur investment and create jobs.

These initiatives focus on boosting domestic manufacturing, especially in electronics and mobile devices, through incentives, subsidies, and regulatory reforms. This strategy has successfully attracted major smartphone manufacturers, creating jobs and fostering technology transfer.

CONCLUSION:

India's shift towards a full design-to-development model in electronic manufacturing is a promising stride, but it's important to remember that the path ahead is still long. While the buzz around manufacturing is encouraging, it's crucial not to get carried away prematurely. Sustaining this transformation will require consistent efforts in research and development, infrastructure enhancement, and skill development. By staying committed to these objectives, India can solidify its position in the global electronic manufacturing landscape and chart a successful course for the future.

India’s EMS sector has also seen a similar rise with recent IPOs and veterans in this sector rising multifold times. Though we remain constructive on the sector, a key thing to watch out for is the transformation of the Indian EMS companies to a full-scale design-to-development manufacturer from an assembler as that would help in the development of a competitive moat. One should also consider the valuations at which these companies are trading. Outliving the recent euphoria, one should discount the company's future growth rate and cash flows over the long term to determine the sustainable multiples for these companies.

We continue to look out for interesting opportunities in this sector by granular understanding of the business model and its competitive strengths and moats.

AMBIT COFFEE CAN PORTFOLIO

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 12 - Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of October 31st 2023; All returns are post fees and expenses; Returns above 1 year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

* Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI

Exhibit 13 - Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of October 31st 2023; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

* Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI.

AMBIT GOOD & CLEAN MIDCAP PORTFOLIO

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

-

Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

-

Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

-

Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 14 - Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of October 31st 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap strategy and the same is reported to SEBI.

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of October 31st 2023. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap strategy and the same is reported to SEBI.

AMBIT EMERGING GIANTS PORTFOLIO

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 16 - Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of October 31st 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants strategy and the same is reported to SEBI.

Exhibit 17 - Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of October 31st 2023. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants strategy and the same is reported to SEBI

AMBIT TENX PORTFOLIO

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follows

-

Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

-

Key driving factors: Low penetration, strong leadership, light balance sheet

-

Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

-

No Key-man risk: Process is the Fund Manager

Exhibit 18 - Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of October 31st 2023; Returns are net of all fees and expenses *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

Exhibit 19 - Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of October 31st 2023. Returns are net of all fees and expenses *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

For any queries, please contact:

Umang Shah - Phone: +91 22 6623 3281 | Email - aiapms@ambit.co | Registered Address: Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013 | Corporate Address: Ambit Investment Advisors Private Limited - 2103/2104, 21st Floor, One Lodha Place, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020. Performance is net of all fees and expenses. Past performance is not a reliable indicator of future results. Please note that performance of your portfolio may vary from that of other investors and that generated by the Investment Approach across all investors because of 1) the timing of inflows and outflows of funds; and 2) differences in the portfolio composition because of restrictions and other constraints. For comparative Performance relative to other Portfolio Managers within the selected Strategy, please visit: bit.ly/APMI_PMS

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/ graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or